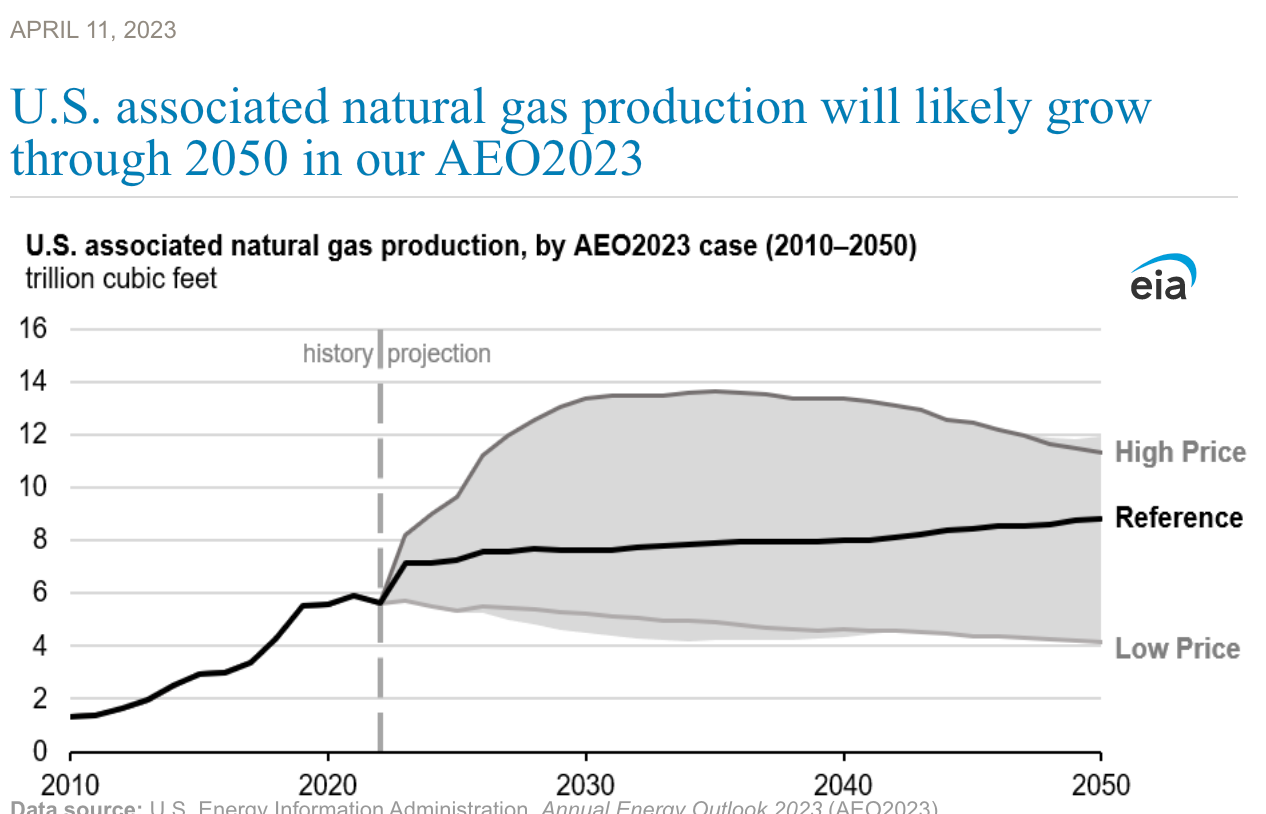

Energy Factoid: EIA projects increased associated gas production through 2050

This puts downward pressure on domestic natural gas prices which is good for consumers and power grids that bring on more natural gas power generation to backup unreliable wind and solar power

Energy Information Administration (EIA) published its projection for 2050 of associated natural gas production on April 11, 2023. Early the next day, Doomberg published an excellent article on Substack, highlighting the importance of associated natural gas and its flaring due to inadequate gas pipeline capacity out of the Permian Basin. This article is a must-read.

My inner economist compels me to make a few observations about associated gas. Since the wells producing associated gas were drilled to produce crude oil, the marginal cost of associated natural gas is zero. That gas is essentially free but must be dealt with to produce crude oil. The gas must either be sold or flared. Venting is usually not a good option due to safety concerns and regulations.

As Doomberg highlighted, a significant amount of associated gas is being flared in the Permian Basin in West Texas, the largest crude oil field in the U.S. and the second-largest globally, due to inadequate gas pipeline capacity to move it to market. If this gas is not flared, the crude oil wells would have to be shut-in, and neither the producers nor the Texas Railroad Commission of Texas (RRC) wants that to happen. Therefore, the RRC allows the associated gas to be flared as an “emergency” matter until additional pipeline capacity is built.

Five gas pipeline projects in the Permian Basin will provide additional pipeline capacity and reduce flaring. Four projects were announced late last year, and one is under construction. Of the four new projects, three will expand the capacity of existing pipelines, and one will be a new pipeline.

The three capacity expansion projects are:

The Gulf Coast Express Pipeline Expansion, announced by Kinder Morgan on May 16, 2022, will expand compression on the pipeline, increasing capacity by 0.57 Bcf/d to 2.55 Bcf/d. The project is expected to enter service in December 2023.

The Permian Highway Pipeline Expansion, which reached a final investment decision by Kinder Morgan on June 29, 2022, will also expand compression, increasing capacity by 0.55 Bcf/d to 2.65 Bcf/d. The project is expected to enter service in November 2023.

The Whistler Pipeline Capacity Expansion, announced on May 2, 2022, by WhiteWater and MPLX, is a joint venture between Stonepeak and West Texas Gas, Inc., that will expand compression by installing three new compressor stations on the pipeline, increasing capacity by 0.5 Bcf/d to 2.5 Bcf/d. The project is expected to enter service in September 2023.

The new pipeline project is:

The Matterhorn Express Pipeline is a joint venture among WhiteWater, EnLink Midstream, Devon Energy Corp, and MPLX. This pipeline will be 490 miles long and will be able to transport up to 2.5 Bcf/d of natural gas from the Waha Hub in West Texas to Katy, Texas. The pipeline will receive natural gas from upstream Permian Basin connections and direct connections at processing facilities in the Midland Basin before connecting to the Agua Blanca Pipeline. The pipeline is expected to enter service in the third quarter of 2024.

The fifth pipeline project is the Energy Transfer Oasis Modernization Project, which came online recently.

Together, these five projects will increase the gas pipeline capacity out of the Permian Basin by a combined 4.18 billion cubic feet per day (Bcf/d) over the next two years. As this additional natural gas comes to the market, it will exert downward pressure on natural gas prices because its marginal cost is zero. As a result, crude oil producers will sell all they can but will be willing to give it away or even pay to have it taken away, that is, sell it for negative prices, to keep the crude oil flowing.

Bottom line: The EIA projection that associated gas will account for 20% of total U.S. production until 2050 is a projection of potentially soft domestic natural gas prices. While this is not ideal for shale gas producers, it is good news for power grids that need natural gas-fired power generation to offset the destabilizing effects of wind and solar. Of course, the international LNG market is continuing to develop, which will be a good market for U.S. natural gas for decades to come.